- Jo Earlam

- June 17, 2023

- 2:28 pm

- 10 min read

Big brothers head higher on supply concerns. Cotton does not have that problem!

Genes are what one is born with and cannot be changed! Understanding oneself and implementing discipline is the path to contentment! In turn, it may determine one's future!

CTN23 81.46 (+0.82)

CTZ23 80.10 (+0.50)

CTH24 80.20 (+0.49)

CTK24 80.47 (+0.41)

CTN24 80.70 (+0.37)

Zhengzhou WQU23 – 16,860 (unch)

Cotlook “A” Index – 91.80 (-0.95)

Daily volume – 29,229

AWP – 67.00

Open interest – 171,169

Certificated stock – 19,472

N23/Z23 spread – (1.36)

Z23/H24 spread – (-0.10)

H24/K24 spread – (-0.27)

K24/N24 spread – (-0.23)

July Options Expiry – 9th June 2023

July 1st Notice Day – 26th June 2023

December Options Expiry – 10th November 2023

December 1st Notice Day – 24th November 2023

Introduction

– There is only a week until July futures need to be cleared up, noting it is a holiday in the USA on Monday, with any remaining fixations needing be cleared up in the next 4 trading days.

– Open interest in N23 is down to just 13,384 contracts against new crop Z23 at more than 10x that figure. N23 dropped 258 points over the week to close at 81.46 having traded in a 377 point range between 80.50 and 84.27. Average futures volume was 40,728 futures daily with overall open interest down to 171,169 contracts and back down at the levels of nearly 2 months ago!

– The front month Z23 was rather less volatile trading between 79.05 and 82.11 being a 306 point range and falling 172 points over the week. This was interestingly the lowest weekly close in 3 months, albeit by just 5 points! An average daily intraday range of 124 points for the week is significant for the fact that it gives us all an insight as to what to expect in the season ahead. In other words a seasonal range that is much lower than normal!

– Another matter to consider is the cost of insurance i.e. options. This was something that back in November last year was extremely expensive as prices fell. Selling insurance to others back then, whilst deemed to be foolhardy, was in fact hugely profitable especially if one was sure we would come back to historical levels of volatility!

– EAP’s comment from the weekend report of the 3rd December last year stated …”As always we like to revert to history and statistics as to clues of what happens next. In short, noting the market has been confined to a 70.10 to 90.52 low to high range since the end of September, we are fairly sure that the intraday volatility is about to calm down a lot, noting that history shows that prices ALWAYS eventually revert back to their mean!”

– Today implied volatility in Z23 is 21.27% meaning price protection is below its 5 year average. i.e. protection of a position TODAY using options is actually very cheap!

– At EAP, we now like to look at a 17 month season beginning 1st January of a calendar year all the way through to the 31st May of the following year, but only look at futures months of the same season i.e. Z23, H, K and N24 only. This means we (and our clients) have an insight that others do not tend to consider and therein lies an advantage!

– The calendar year range so far has seen Z23 trade between 77.56 and 86.98 or 9.42c/lb which considering the previous two seasons which ranked 2 and 4 “most volatile” out of over 60 years of collated data we currently have on record (see immediate chart detailed below), makes the current season likely to be one of the smaller ranges!

– We strongly believe we have already seen the 23/24 seasonal high back in January and a low in the 60’s is quite possible, albeit one that will be all too brief!

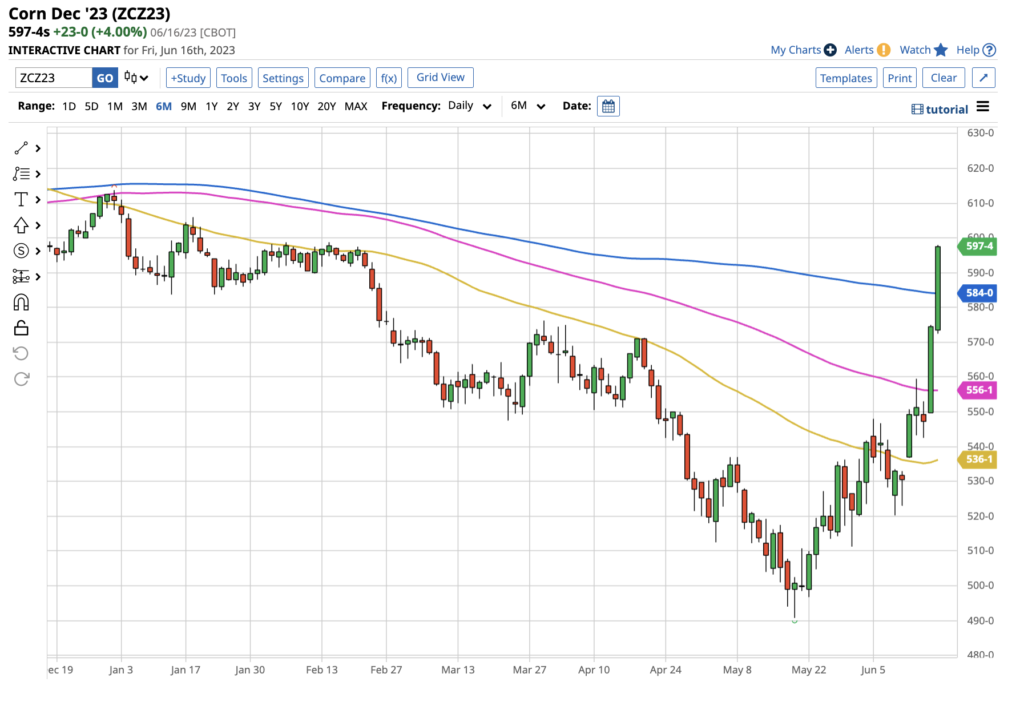

– The three other charts below are of Wheat, Corn and Soy and detail how they have powered higher in the last 3 to 4 weeks. More on that later in this report!

– The chart of Z23 detailed below makes for a range of 69.82 to 95.00 since its inception. This is a range of 25.18c/lb and long term readers of this report will already know that this is a movement that is nothing out of the ordinary!

– Technically speaking and looking at the fibonacci lines detailed in the chart we can see 79.44 is a fairly crucial area and below that the mid 70’s beckons. We feel it is only a matter of time before this lower level is tested despite the support that the big brothers are offering at the present time!

– They have risen fast, since bottoming nearly 3-4 weeks ago. Corn, Soy and Wheat are up 22%, 18% and 19% respectively, whilst Cotton has moved 2%…. yes just 2%! Sceptics on our Cotton viewpoint will rightly point out we often state that “all boats rise with the tide” so why won’t Cotton go up and surely will only be a matter of time before it joins the party?

– In Cotton, we do not face supply issues in the season ahead ….in fact we have too much Cotton and an over stated demand by the USDA. Any “algo” trading on USDA figures might need to readdress the data their model relies upon! In truth there must be a few algo models out there reliant on such information. The COT report from Friday shows funds (MM, OR & NR) still own a net long in Cotton!

– The CFTC COT report for Cotton as of last Tuesday show MM, OR and NR to now hold a net long of 19,121 contracts. This is not an onerous position but we suspect is slightly underwater in view the recent roll from old to new crop and noting Friday’s close for Z23.

– For Corn, Soy and Wheat funds were net short a month ago and the crop concerns was also powered by funds taking their net short to flat or long as they are today. As to whether the big brothers keep going may in part be down to what the funds do next in these markets, which we can only second guess!

– As a final thought, the writer has spent the last week in one of his favourite Cotton growing markets in the world! Greece is a top 10 producer of Cotton in the world and this year there are concerns for the crop, which is planted late!. It is unusually cold here or this time of year and wet! Right now, most think a crop of only 250-260k mt is likely.

– Like the rest of the world (ROW), new crop sales are low and total no more than 15-20k mt, despite the lowest basis in a couple of years at 500-750 points on FOT Greece with a rollover of 25-30k mt of old crop. Merchant buyers are at 400 on for shipment 10/11/12-23 and not in a hurry! Turkey will come to the market as it always does, but it is not happening just yet!

Conclusion

Our efforts remain solely on new crop Z23 which has traded between 77.56 and 86.98 so far this calendar year. EAP suggest this contract is fully valued in the mid to high 80’s and maintain that end users should only consider a scale down long and/or “on call” fixations from the mid 70’s, to maybe into the 60’s at some point!

Useful links

*Please note that we only share CFTC CTO on weekend reports.

Written by:

Jo Earlam

Copyright statement

No image or information display on this site may be reproduced, transmitted or copied (other than for the purposes of fair dealing, as defined in the Copyright Act 1968) without the express written permission of Earlam & Partners Ltd. Contravention is an infrigement of Copyright Act and its amendments and may be subject to legal action.

Disclaimer

The risk of loss associated with futures and options trading can be substantial. Opinions set forth herein should not be viewed as an offer or solicitation to buy, sell or otherwise trade futures, options or securities. All opinions and information contained in this email constitute EAP’s judgment as of the date of this document and are subject to change without notice. EAP and their respective directors and employees may effect or have effected a transaction for their own account in the investments referred to in the material contained herein before or after the material is published to any customer of a Group Company or may give advice to customers which may differ from or be inconsistent with the information and opinions contained herein. While the information contained herein was obtained from sources believed to be reliable, no Group Company accepts any liability whatsoever for any loss arising from any inaccuracy herein or from any use of this document or its contents. This document may not be reproduced, distributed or published in electronic, paper or other form for any purpose without the prior written consent of EAP. This email has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. For the customers of EAP, this email is produced exclusively for our business and expert clients, it is not for general distribution and our services are not available to private clients. Past performance is not indicative of future results.