- Harry Bennett

- November 21, 2022

- 2:23 pm

- 10 min read

Are the funds heading for the exit?

Indices

Futures

Forex

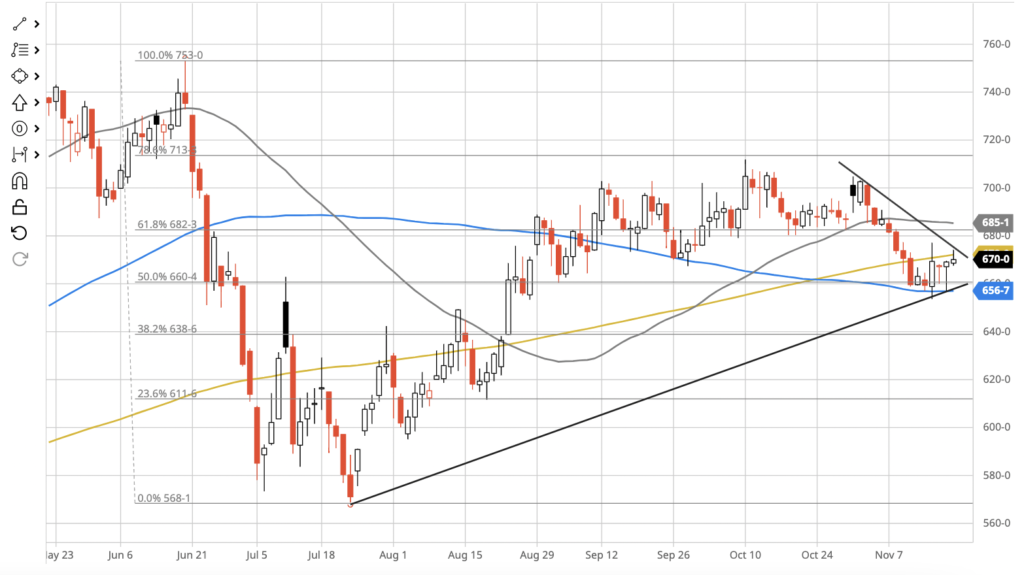

– March Corn’22 (ZCH23) – March Corn futures find support at the 50 day moving average around 566.00 basis ZCH23. The effective front month traded within a 23.60 cent range between 653.40 and 677.00. A narrow trading range as the market bounces between the 50 & 61.8% Fibonnacci retracement levels (660.40 and 682.30 respectively).

– The market seems to be trading within a contracting triangle but looks to be favouring the upside. Either way a move above or below the short term support and resistance levels will set the stage for a break out.

– The front month March contract traded within a 23.60 cent between 653.40 and 677.00. Futures volume diminished throughout the week with a daily average of just 369,804 contracts. Open interest has also declined as we approach December expiry, total open interest now stands at 1,397,090 contracts.

– The CFTC commitment of traders report revealed the managed money had reduced their net long position by 60,831 contracts. Their position now stands at 176,831 contracts net long which is their smallest long position since the 16th August 2022 (see table below).

– U.S. Corn export sales surged last week, for the period between November 4th – 10th 2022 sales totalled 1.169 million mt. Mexico were once again the leading buyers (919,800mt) followed by Canada (91,300mt) and Saudi Arabia (65,000mt).

– In its daily reporting the USDA also announced that private exporters had sold 1,866,900 mt of corn to Mexico on the 16th November 2022. This was the 5th largest daily export sale on record, a full list of the largest daily export sales has been provided here.

– Corn use estimates for ethanol total 779 million bushels so far this year which is down by 67 million (7.9%) from last years pace. However, ethanol production rose for the fifth consecutive week to 1,040k barrels a day last week.

– CFTC Commitment of Traders – Hedge funds appear to be heading for the exit as the managed money reduce their net long position by 60,831 contracts, their overall position now stands at 176,831 contracts net long.

– U.S. corn and soybean harvest is nearly complete, 93% and 96% respectively. Both are ahead of normal pace for this time of the year.

– Drought and heat has taken a toll on the 2022 Corn crop, the USDA estimates yields will be down 12% in the Mid-South. You can see from the map below the significant stress that is see in the high plains region. A link to the full interactive map has been provided at the bottom of this email.

– Grains and beans were higher on Friday as dry weather persists in much of the U.S. Southern plains. It is reported that Winterkill is possible in certain states like Nebraska as temperatures drop far below zero and winds pick up.

– However, despite the drought prices may come under pressure as the Black Sea grain initiative which was meant to expire on Saturday has been extended by four months. This is positive news for the Asia-pacific region as they would be facing much higher prices and lower availability of meat without this extension.

– US Drought monitor (November 17th 2022) – High stress in major growing areas, in particular the high plains. Nebraska state showing exceptional drought in certain locations across the state.

– Ukraine are expected to export 11 mmt of wheat this year along with 15.5 mmt of Corn. If the USDA are correct in their predictions the figures would be down from 18.8 mmt of Wheat and 27 mmt of Corn from the prior season.

– Argentina has seen decent rains over the past week which has been a boost for the corn crop. However, over the next two weeks the country is expecting to see a shift back to drier weather over the next two weeks with 40-60% of normal precipitation expected to be seen.

– Patchy rains will keep corn and soy healthy in Brazil, whilst the more vulnerable Southern regions will be mostly dry which poses a risk to planting and germination (map below). Brazilian corn is still reportedly trading at a $1.00 discount to the U.S. on an FOB basis.

– Brazilian exporters have finally received permission from Chinese customs to supply corn to the country which will directly impact the export of corn from Ukraine & the U.S. The Chinese government updated the list of approved Brazilian corn exporters which includes over 130+ entities.

– 6- 10 day precipitation model – Rains shift Northeast this week and towards the rest of country what will this mean for planting?

Conclusion

The weather premium for U.S. market is firmly in place as yields may be reduced further due to persisting droughts. We may see more downgrades and reductions in both the U.S., China and Europe if the adverse weather continues. The funds have really axed their long position which could be the catalyst to move this market lower. The extension of the Black Sea grain initiative is not supporting the bulls as export flows look to be sturdy. A decisive move above key resistance levels and contracting triangle is needed to bolster this bullish tone.

Written by:

Harry Bennett

Copyright statement

No image or information display on this site may be reproduced, transmitted or copied (other than for the purposes of fair dealing, as defined in the Copyright Act 1968) without the express written permission of Earlam & Partners Ltd. Contravention is an infrigement of Copyright Act and its amendments and may be subject to legal action.

The risk of loss associated with futures and options trading can be substantial. Opinions set forth herein should not be viewed as an offer or solicitation to buy, sell or otherwise trade futures, options or securities. All opinions and information contained in this email constitute EAP’s judgment as of the date of this document and are subject to change without notice. EAP and their respective directors and employees may effect or have effected a transaction for their own account in the investments referred to in the material contained herein before or after the material is published to any customer of a Group Company or may give advice to customers which may differ from or be inconsistent with the information and opinions contained herein. While the information contained herein was obtained from sources believed to be reliable, no Group Company accepts any liability whatsoever for any loss arising from any inaccuracy herein or from any use of this document or its contents. This document may not be reproduced, distributed or published in electronic, paper or other form for any purpose without the prior written consent of EAP. This email has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. For the customers of EAP, this email is produced exclusively for our business and expert clients, it is not for general distribution and our services are not available to private clients. Past performance is not indicative of future results.