July Options Expiry – 10th June 2022

July 1st Notice Day – 24th June 2022

September Options Expiry – 19th August 2022

December Options Expiry – 11th November 2022

December 1st Notice Day – 23rd November 2022

Introduction

– The market suffered a large reversal today, along with the stock markets, closing down the 6 cent limit basis the lead July ’22 contract. Interestingly, the collapse came following a brief spike higher on the back of a strong export report (more on that later!). We have long opined that the market is fully valued, but it is also true that bull markets will exhale from time to time. We will see over the coming days if today’s down move is part of a larger correction.

– The Fed yesterday, as widely expected, increased the base rate by 50 points. This is the largest single increase since May 2000 as the Fed attempts to catch up with runaway inflation.

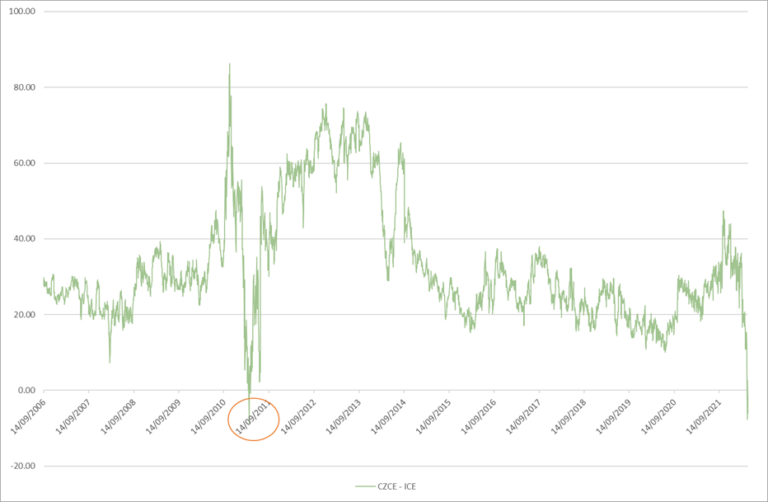

– In another example of the ICE rally exceeding conditions in consuming markets we are now looking at a negative CZCE / ICE cotton spread as can be seen in the chart below. In fact, the only other time that this spread has been in negative territory was April 2011 (there’s that year again!!!).

– NB all of the below charts are based prices prior to today’s change as we will, doubtless, see a reaction in tomorrow morning’s Chinese prices on the open.

– Even more illuminating is the spread between the CC Index and the Cotlook A Index. The below chart goes back to 2015 and, in this period, the Chinese physical cotton price has consistently traded at a premium to the international price, that is until now. (As an aside, this chart is based on a straight conversion and does not account for Chinese import taxes which would add a further premium to the international price).

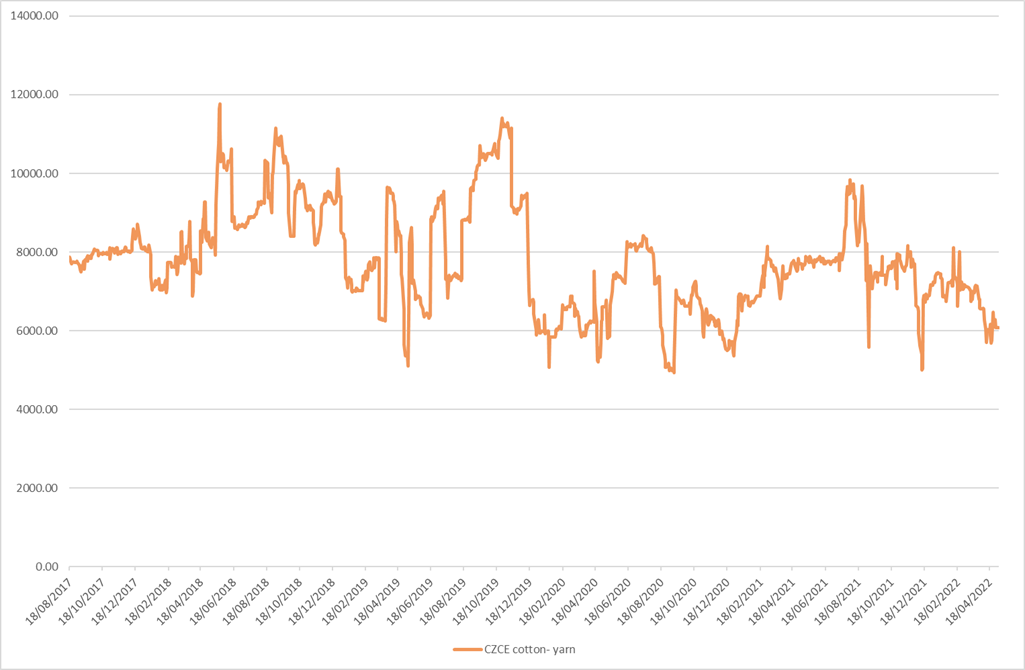

– Finally, as can be seen in our next chart, judging by the CZCE cotton and yarn futures spread, this imbalance between international and Chinese cotton prices has come about whilst the Chinese cotton and yarn prices are not out of line with what could be considered their “normal” range.

– The CFTC Cotton-on-Call report, based positions as of 29th April, showed a small draw down in July ’22 positions of just over 3,000 contracts. The net on call sales position in July stands at 57,329 contracts which remains alarmingly high. Unfixed mills should be taking advantage of today’s weakness to reduce their risk and not gambling on “perfect” prices to come!!

– Irrespective of the above economics, China allegedly bought 113,200 bales gross and 99,700 bales net for the 2021/22 crop year in the week ending 28th April. The simple question would be, why would any Chinese mill buy imported cotton for nearby, amidst a severe lockdown, when they can buy local cotton more cheaply??? Even if the purchases were politically driven then new crop would be a much more logical place for these purchases given the relative price. Overall, net sales totalled 232,400 bales and exports were an encouraging 426,600 bales.

Conclusion

The continued flare up in N22 we cautioned against last week continued in the early part of this week, only to close limit down today after yet another new life of contract high at 155.95. Involvement in N22 is something to avoid if possible, but for new crop December we maintain this contract is very fully valued and the spike in N22 has offered a golden opportunity to lock in a good proportion of new crop sales 25c/lb higher than one could get just 6 weeks ago.

Useful links

*Please note that we only share CFTC CTO on weekend reports.

No image or information display on this site may be reproduced, transmitted or copied (other than for the purposes of fair dealing, as defined in the Copyright Act 1968) without the express written permission of Earlam & Partners Ltd. Contravention is an infrigement of Copyright Act and its amendments and may be subject to legal action.

Disclaimer

The risk of loss associated with futures and options trading can be substantial. Opinions set forth herein should not be viewed as an offer or solicitation to buy, sell or otherwise trade futures, options or securities. All opinions and information contained in this email constitute EAP’s judgment as of the date of this document and are subject to change without notice. EAP and their respective directors and employees may effect or have effected a transaction for their own account in the investments referred to in the material contained herein before or after the material is published to any customer of a Group Company or may give advice to customers which may differ from or be inconsistent with the information and opinions contained herein. While the information contained herein was obtained from sources believed to be reliable, no Group Company accepts any liability whatsoever for any loss arising from any inaccuracy herein or from any use of this document or its contents. This document may not be reproduced, distributed or published in electronic, paper or other form for any purpose without the prior written consent of EAP. This email has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. For the customers of EAP, this email is produced exclusively for our business and expert clients, it is not for general distribution and our services are not available to private clients. Past performance is not indicative of future results.