- Jo Earlam

- July 3, 2022

- 9:26 pm

- 10 min read

Will 22/23 season repeat a similar price action to the 11/12 season?

It is amazing what you can accomplish if you do not care who gets the credit.

CTN22 – 103.68 (-0.26)

CTZ22 – 97.48 (-1.36)

CTH23 – 93.37 (-1.41)

CTK23 – 90.90 (-1.57)

CTN23 – 88.43 (-1.64)

Zhengzhou CF209 – 17,350 (-130)

Cotlook “A” Forward Index – 114.95 (+4.00)

Daily volume – 35,761

AWP – 116.83

Open interest – 175,609

Certificated stock – 13,733

Dec/Mch spread – (+4.11)

July 1st Notice Day – 24th June 2022

September Options Expiry – 19th August 2022

December Options Expiry – 11th November 2022

December 1st Notice Day – 23rd November 2022

Introduction

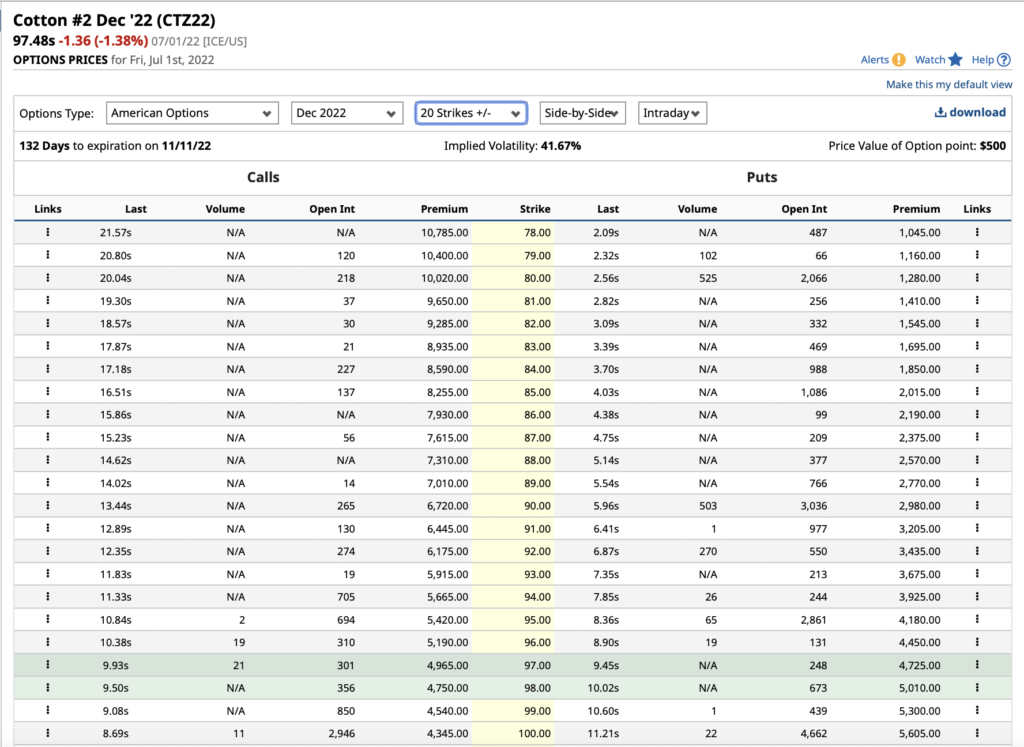

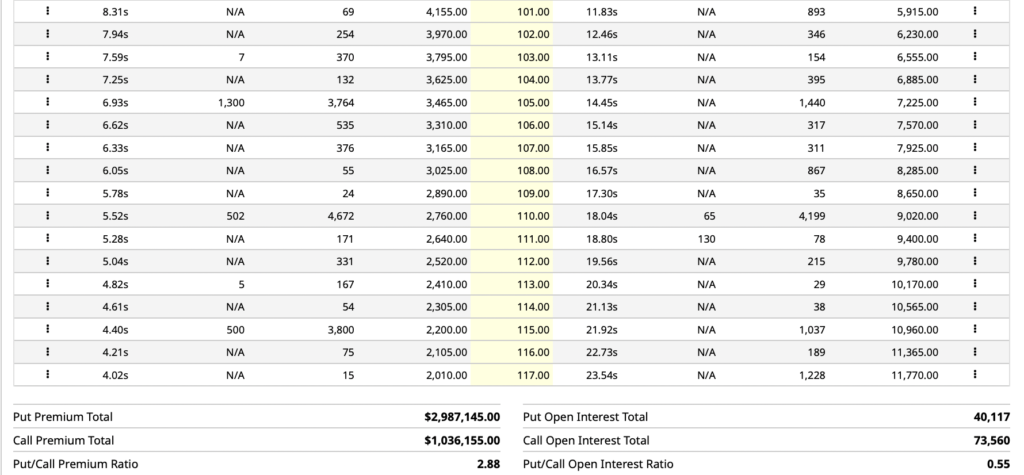

– Cotton had a much less volatile week trading in a 829 point range in the nineties between 91.20 and 99.49. Volume was much lower but still averaged a robust 38,066 futures daily. Options were also active with an average 12,777 options trading daily with call activity outnumbering puts by more than 2 to 1!

– Implied at the money option volatility (cost of buying protection) remains very high at nearly 42% and reflects the fact there is a high degree of uncertainty in where Cotton goes to next! We have once again included details of the open interest for December options which still shows a skew to the “out of the money” calls over puts. i.e. “out of the money” calls remain more expensive than the comparative “out of the money” puts.

– The CFTC COT report showing traders positions as of last Tuesday, saw Managed Money (MM) as big sellers of a net 14,372, taking their net long to 46,738 contracts. Other Reportables (OR) bought a net 3,442 and Non Reportables (NR) sold a net 1,614 contracts. Between MM, OR and NR, they now hold a net long of 62,229 contracts or 6.22m bales. As suggested last week, there have been substantial reductions in their long position and for those who do not think the market can drop further look no further than the fact that funds remain very long and wrong.

– This particular point is extremely important and means that any rallies are likely to see plenty of fund selling. For that reason it is hard to get friendly to this market especially whilst yarn stocks are building and the economic outlook in the 3rd and 4th quarter looks less than rosy.

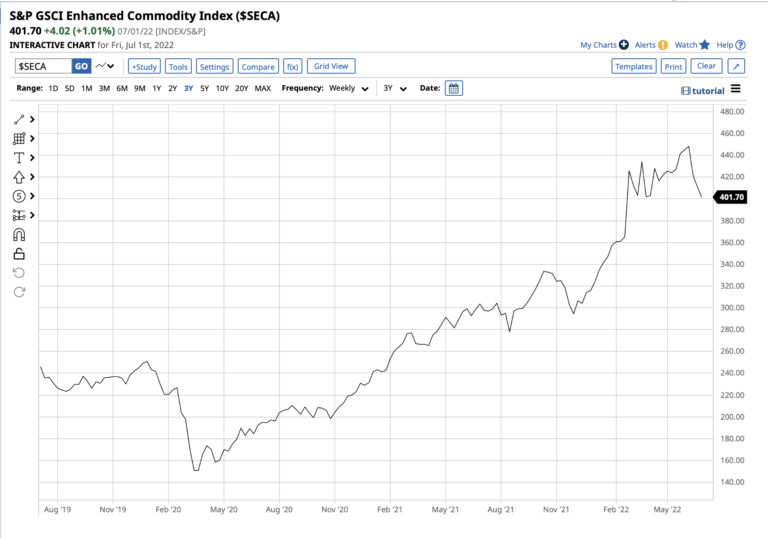

– The GSCI Commodity Index below shows the first substantial drop in over 2 years and a drop of more than 10% in less than a month. We think there is more downside to come across all the commodity sectors!

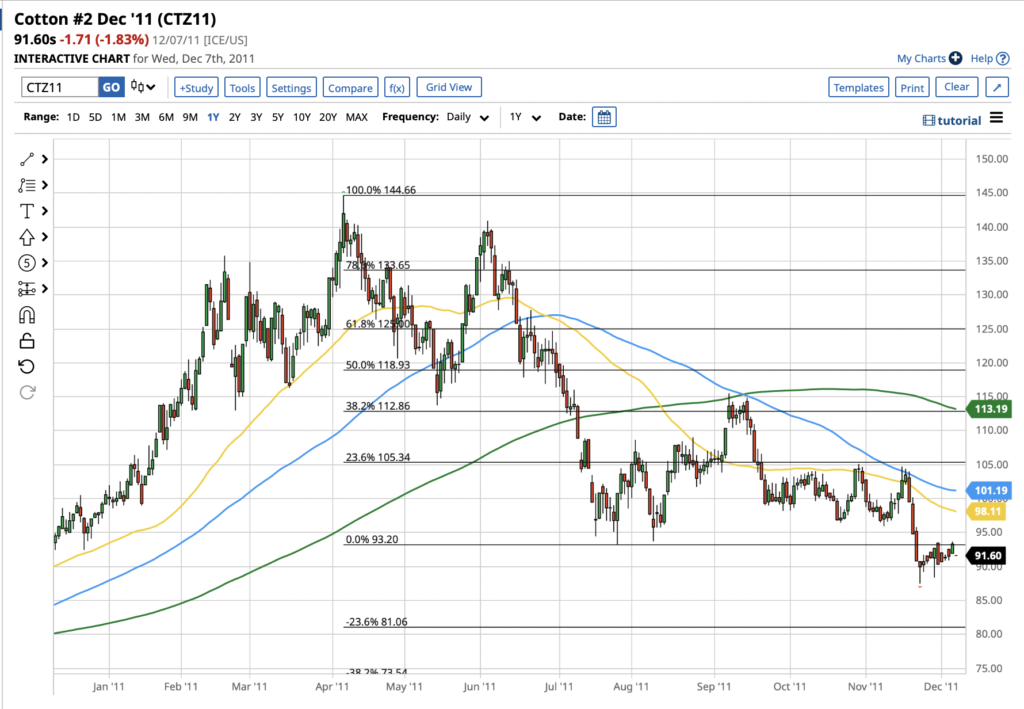

– The uncanny relationship between Z11 and Z22 gives us an excellent insight into what to expect next! Back in 2011 we saw a collapse in Z11 just as we have seen in Z22. The subsequent rally saw a 38.2% to 50% retrace of the fall which spectacularly failed into a hurricane inspired rally into the middle of September.

– This means that for the current season we can possibly hope for a rally to between 102 to 107c/lb or at best an intraday spike to perhaps 110-112. Either way and assuming it were to happen it should be a cracking opportunity to load up on bearish optionnstrategies for what we are quite sure will be an inverse season! The 2nd and final chance to get short if you like!

– Take a look at the N12 chart which offered a shorting opportunity in mid September at 108.50 before eventually seeing prices reach their seasonal low at about 70c/lb by the following May.

– Note how in the 11/12 season the Z12 contract closed at its lows and how between January and April the contract largely moved sideways to lower and traded between 80 and 95 for effectively 4 months before collapsing in the May.

– In truth, before the final move down in May, the pattern was largely sideways as the above cotton continuation chart of the 11/12 season shows!

– If we are right then expect the spreads to narrow into even between H, K and N23 and see carry come back into the market for the 23/24 season which is exactly what happened in the 11/12 season.

– On a macro point of view the 2nd quarter of 2022 has ended on a rather sour note. Only the energy sector closed higher than the end of Q1 but precious and base metals, grains and soft commodities all moved to the downside in Q2. Cryptos were the ugliest, where the market cap of the sector dropped 60%…Crikey!

– We have rising interest rates, the strongest dollar in 2 decades and this is weighing on raw material prices which will hopefully cause inflationary pressures to recede over the coming weeks and months.

– Expect market liquidity to decline in the 3rd quarter as summer vacations will mean lower market participation especially in July and August. The huge drop in the Copper price known to be a barometer of the world economy is signalling a recession has already begun. A negative reading on Q2 GDP will confirm the economic condition.

– We can expect lots of market volatility in the 3rd quarter of 2022!

Conclusion

We think the market has found a short term bottom at 91.20 but if retested, 88 to 89c/lb will also be strong support. Above the market, we see stiff resistance in the early 100’s up to 110c/lb and if we were we to see a rally into this area then we would expect the bear to reassert itself. EAP maintain our viewpoint this will be an inverse season and we have already seen the seasonal high at 133.79c/lb on the 17th May and now think a move to the mid 70’s is likely with timing towards the end of May before the current bear market is over!

Useful links

*Please note that we only share CFTC CTO on weekend reports.

Written by:

Jo Earlam

Copyright statement

No image or information display on this site may be reproduced, transmitted or copied (other than for the purposes of fair dealing, as defined in the Copyright Act 1968) without the express written permission of Earlam & Partners Ltd. Contravention is an infrigement of Copyright Act and its amendments and may be subject to legal action.

Disclaimer

The risk of loss associated with futures and options trading can be substantial. Opinions set forth herein should not be viewed as an offer or solicitation to buy, sell or otherwise trade futures, options or securities. All opinions and information contained in this email constitute EAP’s judgment as of the date of this document and are subject to change without notice. EAP and their respective directors and employees may effect or have effected a transaction for their own account in the investments referred to in the material contained herein before or after the material is published to any customer of a Group Company or may give advice to customers which may differ from or be inconsistent with the information and opinions contained herein. While the information contained herein was obtained from sources believed to be reliable, no Group Company accepts any liability whatsoever for any loss arising from any inaccuracy herein or from any use of this document or its contents. This document may not be reproduced, distributed or published in electronic, paper or other form for any purpose without the prior written consent of EAP. This email has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. For the customers of EAP, this email is produced exclusively for our business and expert clients, it is not for general distribution and our services are not available to private clients. Past performance is not indicative of future results.