CTZ22 – 94.62 – (+0.19)

CTH23 – 92.23 – (+0.28)

CTK23 – 90.84 – (+0.30)

CTN23 – 88.92 – (+0.30)

CTZ23 – 81.76 – (-0.07)

Zhengzhou CF301 – 13,665 – (-225)

Cotlook “A” Index – 113.25 (+0.95) – From the 3rd August 2022

Daily volume – 15,171

AWP – 104.48

Open interest – 188,086

Certificated stock – 4,552

Z22/H23 spread – (+2.29)

Z22/Z23 spread – (+12.86)

September Options Expiry – 19th August 2022

December Options Expiry – 11th November 2022

December 1st Notice Day – 23rd November 2022

– August has begun quietly with many traders either on, or soon to go on holiday and we can expect futures volume to dwindle in the days ahead.

– Indeed, it would be fair to say that the intraday range has already started to get smaller with the last 2 days seeing a range of less than 200 points intraday. If this continues then expect implied “at the money” volatility for Z22 options to go lower!

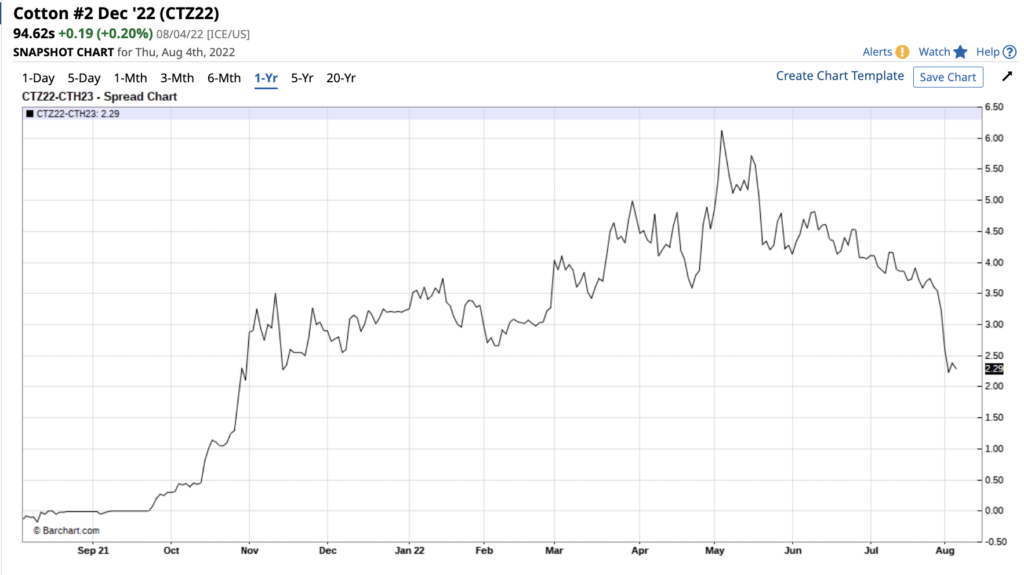

– What is more intriguing is the fact that the spread between Z22 and H23 has finally started to reduce, closing tonight at just 229 points and if prices eventually head South into Z22 expiry, as EAP expect, then one should also expect the spreads between Z22/H, K and N23 to also get much closer. A chart of the Z22/H23 spread is enclosed below!

– Take a good look at how this spread premium has started to implode in the last few days!

– This is exactly what happened in the 11/12 season so if we are right about the current season being a comparable one then one should know what to expect!

– The weekly CFTC Cotton “on call” report 30 showed that between current crop Z22, H, K and N23 there is a net 63,123 contracts to be fixed. Of this amount the majority (60%) is against the front month Z22 contract.

– The current net “unfixed “on call” position in Z22 is the highest ever for week 30 but the net “unfixed” position for the 22/23 season (i.e. Z22, H, K and N23) is certainly not!

– We were rightly reminded today by some insightful traders at a AAA1 merchant house, that many of the forward sales of new crop Cotton are being offered and SOLD by merchants against Z22 for shipments out to 1/2/3-23eq. Moreover, uncovered and short buyers simply have no choice but to buy on such terms!

– The reason for this is merchants realise the tightness of supply right now as well as the logistical problems (read delayed shipments) and continued high freights from many parts of the world.

– Consequently we have a much higher “unfixed” figure for Z22 and a lesser “unfixed” figure than normal for H, K and N23. Note how the December contract closed last week at a premium of 323 points over the H23 contract (i.e. merchants were getting 323 points higher than they would against H23). Normally any sales for 1/2/3-23 eq would be against the H23 contract.

– The weekly USA Export sales report as of July 28th 2022 was disappointing! Net sales reductions of 112,400 RB for 2021/2022 was a marketing-year low and details can be found by clicking on the link below

– In Australia, we hear that the current 2022 crop is no more than 50% ginned and some gins will be operational to as late as November, for a crop (that we are reliably informed) will be 5.5m Australian sized bales. This translates into 5.735m statistical bales (480 lbs).

– We believe 85% of the crop is already sold from farmer to merchant and can only guesstimate what merchants still have in their hands of this most reliable and well regarded growth which is available when most of the Northern hemisphere crops are not!

– Next year we can expect a similar or even larger Australian crop as water seems in plentiful supply!

Prices have held the recent 82.54 low and a counter trend bounce has occurred which could take prices as high as the low 100’s but is expected by EAP to fail. Potentially, a test of the 200 day moving average is possible fuelled by some courageous end user physical buying and/or a hurricane inspired series of events. However, EAP maintain our longer term viewpoint that a final move to the 70’s will eventually play out by next May and the 22/23 season will prove to be an inverted season.

*Please note that we only share CFTC CTO on weekend reports.

No image or information display on this site may be reproduced, transmitted or copied (other than for the purposes of fair dealing, as defined in the Copyright Act 1968) without the express written permission of Earlam & Partners Ltd. Contravention is an infrigement of Copyright Act and its amendments and may be subject to legal action.

The risk of loss associated with futures and options trading can be substantial. Opinions set forth herein should not be viewed as an offer or solicitation to buy, sell or otherwise trade futures, options or securities. All opinions and information contained in this email constitute EAP’s judgment as of the date of this document and are subject to change without notice. EAP and their respective directors and employees may effect or have effected a transaction for their own account in the investments referred to in the material contained herein before or after the material is published to any customer of a Group Company or may give advice to customers which may differ from or be inconsistent with the information and opinions contained herein. While the information contained herein was obtained from sources believed to be reliable, no Group Company accepts any liability whatsoever for any loss arising from any inaccuracy herein or from any use of this document or its contents. This document may not be reproduced, distributed or published in electronic, paper or other form for any purpose without the prior written consent of EAP. This email has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. For the customers of EAP, this email is produced exclusively for our business and expert clients, it is not for general distribution and our services are not available to private clients. Past performance is not indicative of future results.